07/16/2025

PRICE GUIDELINES FOR ICMS-ST CALCULATION ON AUTOMOTIVE BATTERIES

The Equation that Inflates Prices, Erodes Competitiveness, and Increases Informality.

Just like Brazil’s national soccer team, the complexity of the Brazilian tax system is a world champion. One of the tax collection methodologies “made in Brazil” that complicates taxpayers’ lives is the anticipation of ICMS for the entire chain by the manufacturer/importer, commonly known as Tax Substitution or ICMS-ST. To add complexity to this tax collection method, Article 8, § 1, II of Complementary Law No. 87/1996 (Lei Kandir) authorizes states to set the ICMS-ST calculation: “The tax base, for purposes of tax substitution, shall be […] II – the price charged by the substituted party or the Weighted Average Price to the Final Consumer (PMPF), determined by a price survey conducted by the State.” The CONFAZ Agreements (e.g., 110/2007, 13/1994) detail the methodology, and State ordinances periodically update the values.

From the State's perspective, by applying this methodology, its operational efficiency in tax collection reaches its peak due to: cash flow anticipation – the tax is collected at the origin, before retail sale; simplification (for the Tax Authority) – a single presumed base for thousands of taxpayers; ease of auditing – quick comparison between PMPF, rates, and collections; and predictability of revenue – important for states with high budget rigidity.

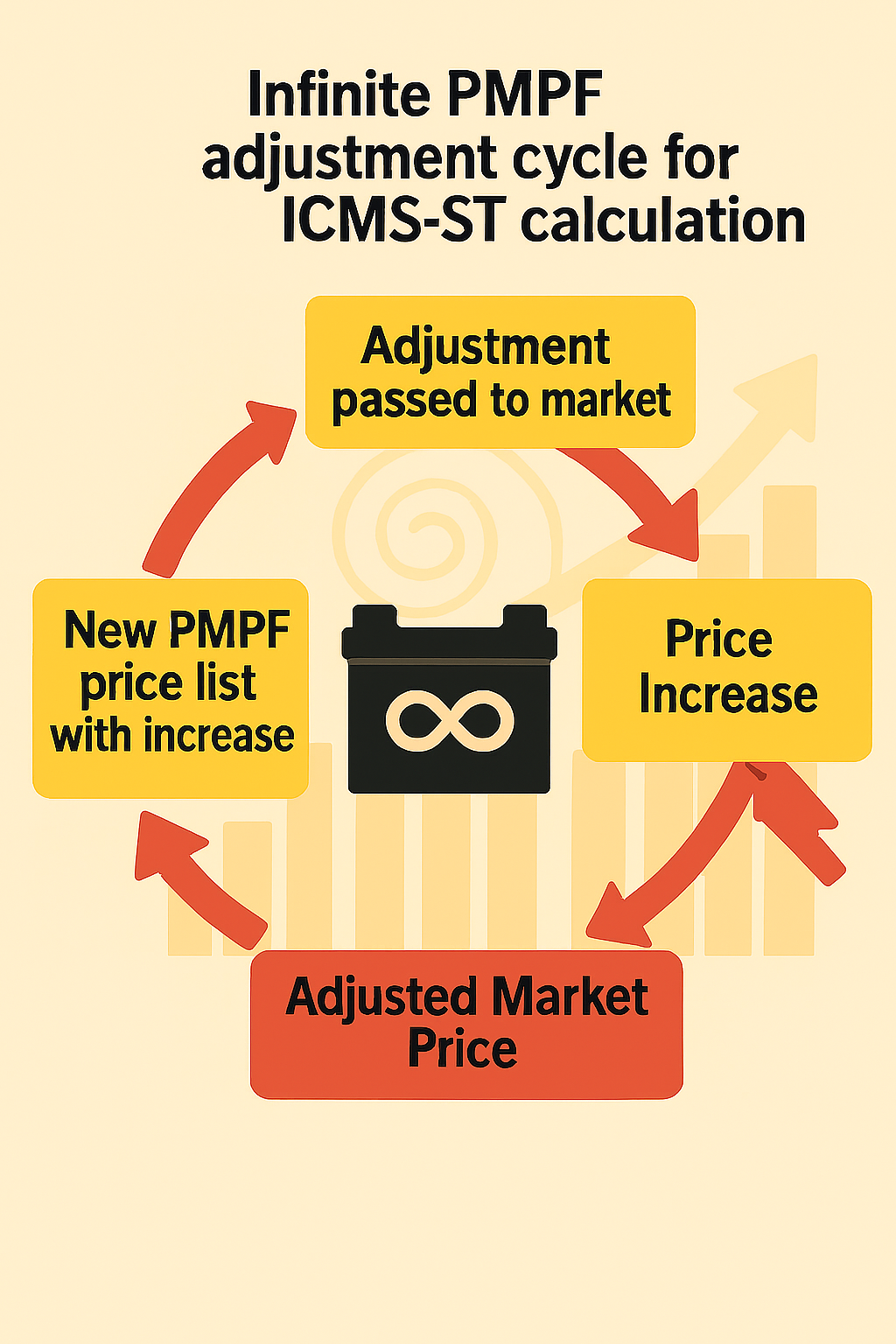

In recent years, SP, MG, MT, MS, and PE have issued successive ordinances increasing the PMPF values for automotive batteries, creating an endless cycle of increasing ICMS-ST charged and calculated using the PMPF methodology. The cycle begins with the publication of the first PMPF Ordinance, which causes a perceived price increase due to the anticipated ICMS-ST. The embedded tax cost is passed on to the final consumer, and price surveys conducted by the State detect the new, higher prices. Every six or twelve months, a new ordinance with even higher PMPF values is published, restarting the cycle. The result is a self-referential inflationary system, not based on real added value or correction indices.

Simulations with 60 Ah and 75 Ah batteries (current ordinances in SP and MG, 18% tax rate) show the retained tax exceeding 40% of the retail price. For premium 90 Ah lines, the burden can reach 50%. In practical terms, half of what consumers pay for some automotive battery models is ICMS-ST.

Industries, in addition to seeing their cash flow drained by the responsibility of tax collection, witness the rise of informality among some competitors. Formal retailers fully bear the retained tax to remain competitive. Meanwhile, tax evaders (who buy and sell without invoices) use the ICMS-ST calculated with the PMPF methodology as profit margin, gaining a huge illicit competitive advantage. The result is disheartening: honest traders must flirt with informality or go under to survive.

But there is light at the end of the tunnel! The states of Santa Catarina, Rio Grande do Sul, Espírito Santo, and Goiás have denounced the ICMS-ST protocol, ending Tax Substitution by either MVA or PMPF methodology for automotive batteries. Let’s look at the data presented by Santa Catarina, which proves revenue did not decline. From April 1, 2020 (Decree 479/2020), the opposite was observed: April 2020 marked the lowest point of the series, affected simultaneously by the end of ST and the pandemic shock. April 2021 already surpassed April 2020 by 78% and stood about 9% above the pre-pandemic level (April 2019). These numbers show that, once the initial impact was absorbed, the debit-credit based tax collection (regular regime) not only compensated for the end of the ST regime but also followed the sector's recovery. In other words, ending ICMS-ST did not result in revenue loss for the State; it merely eliminated a tax advance that historically strained the cash flow of distributors and retailers without ensuring greater fiscal efficiency.

"States and taxpayers will both benefit from the end of ICMS collected through tax substitution," says Átila Bernardes Nunes, a consultant hired by the Brazilian Sustainable Energy Association – ABES and co-creator of the project “Improvements in the Commercial Environment of Automotive Batteries in Brazil.” “The union of all manufacturers has never been more necessary. Together, we must fight to ensure a fairer, more dynamic, sustainable, ecological, and innovative market,” reinforces Nilson Santos, Executive Director of ABES and co-creator of the same project. The support of politicians, businesspeople, commercial partners, and associations is essential, as only through this collective strength will we be able to pressure states and shift the automotive battery sector out of the tax deadlock represented by ICMS-ST, worsened by the PMPF methodology.